The Liverpool Cotton Futures Market

Contents of this page:

- Widespread and Extensive Use of Liverpool Cotton Futures Contracts

- The Purpose of Futures Markets

- The Use of Futures by Those Trading Cotton

- The Factors that Can Lead to the Evolution of a Futures Market and the Existence of these Factors at Liverpool

- Forward Trading of Cotton at Liverpool before the Development of a Futures Market

- The Effects of the American Civil War and its Aftermath: The Emergence of the Futures Market to 1873

- The Uses of Liverpool Futures Contracts

- The Clearing House and the Development of Margins/Differences

1. Widespread and Extensive Use of Liverpool Cotton Futures Contracts

The Liverpool cotton market is remarkable in being the first commodity market in Europe to develop futures trading (sometimes called ‘derivatives’), considerably ahead of the London markets which still trade futures contracts today. By the late nineteenth century, all branches of the British cotton trade – importers, brokers, spinners and weavers - were widely using the Liverpool cotton futures market. For instance, in terms of the industry, in January 1912, the Facit Mill Company of Rochdale stated that its policy was to use Liverpool futures contracts to cover all its supplies of raw cotton (Facit Mill Company Ltd., Directors Minutes, 25 January 1912, in the Lancashire Record Office, Preston: DDX 639/1/2), in the 1890s, the Sun Mill Company of Oldham covered half its supplies of cotton with Liverpool futures (Sun Mill Co. Ltd., Minutes, 8 June 1891, in the John Rylands University of Manchester Library: SM/1/3), other spinning companies, such as John Hawkins & Sons Ltd. of Preston, varied the extent to which they covered supplies with Liverpool futures (see for instance: John Hawkins & Sons Ltd., Directors Minute Book, pages 10-11 and passim, in the Lancashire Record Office, Preston: DDX 868 27/2). In 1904, the industry journal Cotton commented that the practice of merchants importing cotton without using Liverpool futures was ‘defunct’ (Cotton, 17 September 1904, page 9). The size of the Liverpool futures market became such that some Liverpool cotton broking firms actually made more money from brokerage on cotton futures than on the actual physical ‘spot’ cotton itself.

2. The Purpose of Futures Markets

Futures contracts are, in a sense, a form of ‘paper currency’ for a commodity. Futures contracts promise delivery of a set quantity of a commodity at some stage in the future. They have various uses, for speculators they are an ideal instrument because one is dealing in ‘promises to supply’ rather than having to handle the bulky physical commodity. For other, more ‘legitimate’ traders, their value is that they can be used to guard against price changes - this is known as ‘hedging’. For instance, when an importer contracts to buy a commodity overseas he can guard himself against the value of this commodity falling while in his possession, by immediately selling futures contracts. When he comes actually to sell the physical commodity, he buys back his futures contracts (at the then current market price). By so doing, he is guarded against price changes.

3. The Use of Futures by Those Trading Cotton

Cotton merchants, brokers and spinners all came to use the process of ‘hedging’ to safeguard themselves against a fall in the price of their stock. While holding cotton at sea, in warehouses or at their mills, they sold futures contracts against them, with the intention of buying these contracts back when they came to sell or spin their actual stock. A considerable number of those who bought the futures contracts were speculators and hence were not interested in actually having cotton delivered under the futures contracts and were (except in exceptional circumstance) happy to let the seller buy them back. The speculator would, of course, hope that the price of cotton would have risen, so leading to the seller (merchant, spinner or broker) having to pay more to buy the futures contracts back than they were worth when they sold them.

4. The Factors that Can Lead to the Evolution of a Futures Market and the Existence of these Factors at Liverpool

A variety of factors can lead to the development of a futures market. The key circumstances are variability to the point of instability in the price of a commodity, uncertainty and lack of information concerning the scale of supply, the ability to specify a standard grade of the commodity and the existence of a body able to regulate effectively such a market. With few exceptions, futures markets develop out of existing ‘forward’ markets. To clarify the distinction: a forward market is one in which it is a common practice for specific lots of a commodity to be contracted for before they are available for delivery, as opposed to a futures market in which contracts are highly standardized and do not refer to a particular cargo or lot of a commodity (see: Barry A. Goss (ed.), Futures Markets: Their Establishment and Performance, London: 1986, page 1; Barry A. Goss, The Theory of Futures Markets, London: 1972, pages 4-5; Cento G. Veijanovski in Goss (ed.) Futures Markets, Chapter 1. C. W. Morgan, Price Instability, Trade and Futures Markets, Nottingham: 1994), page 7).

The Liverpool cotton market satisfied all these major preconditions. The Liverpool Cotton Brokers Association existed as potential regulatory body. The uncertainty relating to the supply and price of cotton could place those handling this commodity at risk of financial loss, hence they had a desire to find some mechanism that could guard themselves against price fluctuations. There is ample documentary evidence of cotton importers in the first half of the nineteenth century (before the evolution of the futures market) incurring losses due to a fall in the price of cotton while in transit or when holding stocks in Liverpool. For instance in 1841, a sharp fall in the price of cotton caused many importers to incur losses, bringing some to the brink of bankruptcy (Bank of England, Liverpool Branch, Letter Book, 27 July and 7 August 1841, in the Bank of England Archive, London: C129/2, pages 270, 293-4). Early in February of 1842, the Liverpool cotton broker and importer George Holt wrote to his cotton shipping agent in New Orleans: ‘Everybody is losing money & have lost it & with it have lost heart, all traders & importers are poorer’ (George Holt to John Arrowsmith, 3 February 1842, copy of letter in the possession of Nigel Hall). It is interesting to note that in this crisis the credit normally supplied by banks and brokers to assist in the holding of stocks dried up, no doubt due to their nervousness concerning the serious commercial situation (Bank of England, Liverpool Branch, Letter Book, 27 July 1841, in the Bank of England Archive, London: C129/2).

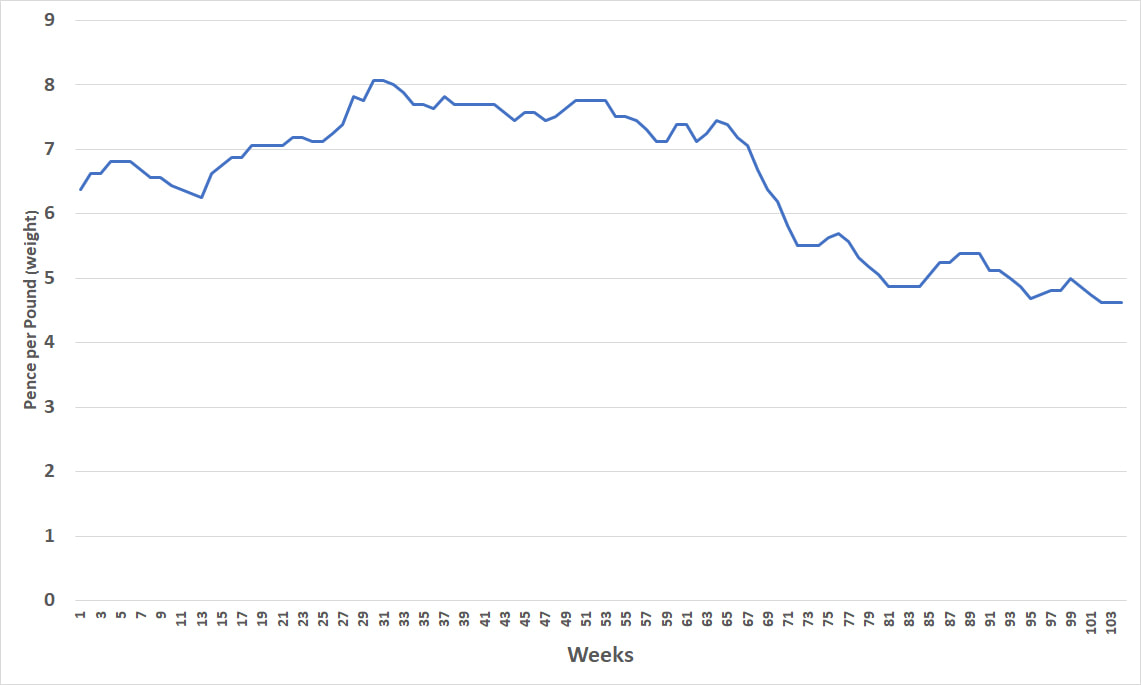

The volatility of the price of cotton can be demonstrated by graph. The graph below indicates the price of middling quality American cotton in Liverpool over two example years, from January1850 to December 1851, emplyoying the weekly price data collected by Liverpool's cotton brokers in the period:

GRAPH:

Weekly Price of Middling Quality American Cotton in Liverpool,

January 1850 to December 1851

Weekly Price of Middling Quality American Cotton in Liverpool,

January 1850 to December 1851

(Source: Weekly Cotton Market Reports (manuscript) in the Liverpool Record Office: 380 MD 130. These reports provide the price of 'Orleans'/American cotton with the price range from 'low middling' to 'middling fair' qualities. The graph above is construced using the median of these two prices)

5. Forward Trading of Cotton at Liverpool before the Development of a Futures Market

A forward market in cotton had developed at Liverpool out of which a futures market could develop. Evidence suggests that forward selling of specific cargoes of cotton certainly took place at various points from the early to mid-nineteenth century in Liverpool. For instance, in the period of high cotton prices and speculation during the War of 1812 between Britain and the United States, the cotton sales book of the Liverpool cotton broker, George Holt, indicates that he traded various lots of cotton before they were landed in the port (for instance George Holt purchased of 150 bales of United States cotton on 26 December 1814, to arrive in Liverpool on or before 26 January 1815. George Holt and Co., Daily Cotton Purchases and Sales Book, 1814-1815, in the Liverpool Record Office: MD 230-9). At around the same time the Liverpool brokers M. & J. Pool were also making forward sales, many months before cotton might be delivered. The firm noted on 15 January 1815 that it had sold fifty bales of American cotton ‘ … deliverable any time before 1 Aug next, to be equal to sample in Campbell’s hands [another broker] & to be paid for in 10 d[ay]s after our notice [with] … good bills on London @ 3 m[onth]s …’ (M. & J. Pool, Journal & Ledger, 15 January 1815, in the Wiltshire Record Office, Trowbridge: 946/283). In less hectic times, in the years following the war, this form of trade appears to have been far less common, with little or no indication of it in the surviving records of Liverpool’s merchants and brokers. There may have been another period of buying cotton before it was landed in Liverpool, associated with the cotton speculations and high cotton prices in the year 1825 (see for instance a court case relating to one such sale in The Liverpool Mercury, 17 March 1826, page 295).

Improved knowledge of cotton shipments which developed in the second quarter of the nineteenth century aided the development of forward selling, particularly through the faster mail ships, especially those of the Cunard line. W. F. Machin (who wrote a short history of the Liverpool cotton market) states that these ships in particular spurred forward selling of cotton (W. F. Machin, ‘A short History of the Liverpool Cotton Market’, in Liverpool Raw Cotton Annual, 1957, pages 257-269). Some surviving evidence, such as the letters of James Brown, a captain of a Liverpool merchant’s ship, indicate how in the 1840s he was able to provide his merchant employer with plentiful information regarding his cotton shipments from New Orleans a considerable time before they were landed in Liverpool, using mail ships. This would have enabled the merchant, John Croft, to trade his cotton in Liverpool before it arrived if he so wished. For instance, on one voyage, Croft’s ship arrived in New Orleans in early October 1844 and sailed for Liverpool around 30 November. While in port in America, Brown wrote five times to Croft in Liverpool advising him of prices in New Orleans and the amount of cotton he had freighted the ship with. It is interesting to note in Brown’s letter of 8 October 1843 that he states he is writing it in a hurry so that the letter can catch the Great Western before it departed for England (Letter Book of James Brown, 8, 19 October, 4, 17, 30 November 1843, in the Liverpool Record Office: 387 MD 48).

In 1857, a conjunction of high cotton prices, speculation and the partial completion of the telegraph to India (permitting knowledge of shipments of Indian cotton) produced a mini-boom in forward trading in Liverpool, and there are numerous references to this in contemporary newspapers and archival sources (see for instance: the Liverpool Daily Post, 14 February 1857, page 8; The Liverpool Mail, 21 February 1857, page 4, 11 July 1857, page 5). This came to a sudden halt in late October 1857 with news of the financial panic of this year in the United States, which spread to Europe, and seriously affected the Liverpool cotton market (Weekly Cotton Market Reports (manuscript), 1857, in the Liverpool Record Office: 380 MD 130).

Forward trading of cotton was therefore taking place in the years before the outbreak of the American Civil War (a period when it grew enormously), but seems to have been most common in times of high prices and speculation. The logical conclusion that much forward cotton was bought by speculators is significant - it is a necessary prerequisite for a futures market that some market operators are willing to adopt a ‘long’ position, in order to buy the futures contracts put out as hedges by those holding stocks of actual, ‘spot’ cotton.

6. The Effects of the American Civil War and its Aftermath: The Emergence of the Futures Market to 1873

The period of extremely high cotton prices and speculation associated with the ‘Cotton Famine’ of the American Civil War (1861-65), followed by generally falling prices over a period of years, provided the conditions which ingrained forward trading and began the process whereby some forward trading of cotton at Liverpool mutated into what we would today recognise as futures trading. The major distinguishing feature between forward contracts and futures contracts is standardization of terms. That is to say, in a futures contract there is a fixed quantity and quality set for the commodity which permits contracts to be bought and sold rapidly between traders who know exactly what it is they are buying and selling (hence, crucially, the market is highly ‘liquid’); only one part of the contract is negotiable - the price (John Buckley (ed.), Guide To World Commodity Markets, 7th ed., London: 1996, page 14. Cento G. Veijanovski in Barry A. Goss (ed.), The Theory of Futures Markets, London: 1972 pages 30-1). The other key point is that under futures contracts, the commodity is rarely (if ever) delivered - the contract is generally bought back at maturity by the seller (Goss, Futures Markets, page 28).

Some forward selling of cotton began in Liverpool almost as soon as the American war broke out (see: Gore’s General Advertiser, 26 September 1861), but it commenced in earnest in 1863, particularly in the autumn, with the price of spot cotton between three and four times the pre-war level due to the war-time shortage. Speculation was spurred by recovering demand for cotton goods from the key Indian market, which had been somewhat glutted with goods around the start of the war. It should be noted that at this stage the forward selling was generally in Indian cotton due to the shortage of the American type, aided by the telegraph communication with the sub-continent. Forward prices for cotton began to be quoted regularly in the Liverpool trade press in late 1863 (Annual Circulars of Cunningham & Hinshaw and John Wrigley & Sons (cotton brokers), 1863, in the Liverpool Record Office: MD 230-22. Gore’s General Advertiser, 1 October 1863. See the reminiscences of the war time cotton trader, Auguste Wiener following the giving of the following paper: S. J. Chapman and Douglas Knoop, ‘Dealings in Futures on the Cotton Market’ in Journal of the Royal Statistical Society, volume 69, (1906), page 365. For information on war time trading conditions at Liverpool see: N. Hall, ‘The Liverpool Cotton Market and the American Civil War’ in Northern History, volume 34 (1998), pages 149-69).

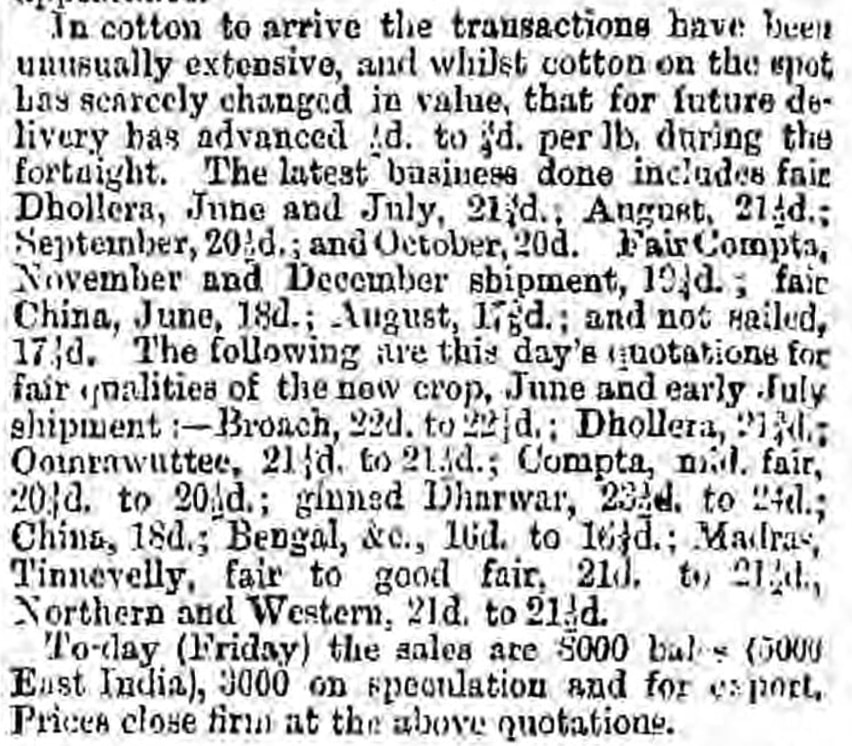

Below:

Part of Liverpool cotton market newspaper report from October 1863

discussing extensive forward trading of cotton

(The Liverpool Mercury, 3 October 1863, page 6)

The names 'Dhollera', 'Compta', 'Broach', 'Oomrawuttee', Tinnevelly' were

varieties of Indian cotton

The forward cotton market in Liverpool moved a step closer to a futures market with individuals beginning to make contracts when they were not in possession of actual cotton, in other words not referring to specific shipments and acting as what we would call ‘bears’. The commencement of this was also noted as taking place in 1863, by the broking firm of Smith, Edwards & Co. (Smith, Edwards & Co.’s Annual Cotton Circular for 1864, in the Liverpool Record Office: MD 230-22). The forward market became what might be termed ‘institutionalized’, again in 1863, through the Liverpool Cotton Brokers Association producing a standard form of contract for traders to use for forward sales – this contract was reproduced and discussed in The Times, on 12 November 1863 (page 6).

There was a reduction in forward trading caused by sharp falls in the price of cotton in the late summer of 1864 (sparked by the raising of the discount rate and rumours of peace in America) but forward trading had become firmly established as a permanent feature in the Liverpool market and continued after the close of the conflict.

The reason for the continued extensive use of forward selling in the years following the American Civil War was the difficult market conditions which Liverpool cotton merchants faced. From the end of the American Civil War and into the 1870s, the international price of cotton steadily fell. This was because of the recovery of the United States after the disruption of the war to its previous level of cotton production. Gradually, year on year, the United States recovered a little more, supplies of cotton increased and prices fell. Merchants importing cotton were therefore at serious and prolonged risk of the value of their cotton stock falling between the date they purchased it in the United States and when they came to sell it in the Liverpool market. The Liverpool merchant, Thomas Bower Forwood, warned his son, William Bower Forwood, in August 1866: ‘ … the most dangerous trade you can go into is cotton, and it will be so for years to come.’(Thomas Bower Forwood to William Bower Forwood, 13 August 1866, in the Hampshire Record Office, Wnchester: 19M62/9/13). Hence, there existed good reason for importers to try to guard themselves against price falls by making forward sales as soon as they had made their purchases in America. Speculators and others purchased the forward sold cotton either to safeguard their future supply or in the hope of profiting if the price of cotton did rise while in transit.

One of the major agents leading to an expansion of forward trading and further advance towards a futures market was the development of telegraph links with the United States, with the cable between Britain and the United States coming into operation in 1866. The cable was very quickly put to use for transferring information relating to cotton across the Atlantic (See for instance the ‘telegraphic cotton report’ in Gore’s General Advertiser, 27 Sept. 1866). Information regarding shipments from the United States to Liverpool could be relayed in a fraction of the time taken by ship, and a similar speed was possible in orders of cotton from Liverpool to the United States.

The notion of specifying a standard quality in contracts appears to have emerged around 1866 and this innovation is usually attributed to the cotton broker John Rew. One of the key problems with forward selling of cotton was uncertainty regarding the exact quality of the cotton. Rew therefore made his contracts on the basis of ‘middling’ quality; the value of any actual cotton delivered would be established in relation to the price of this quality (Todd, Marketing of Cotton, pp. 67-8. Machin ‘Cotton Market’ (1957), pp. 302-4. Auguste Bruckert, Cotton Pamphlet, (Liverpool, 1911) pp. 9-10), (providing the cotton was delivered, rather than the contract being bought back). One finds forward prices in the Liverpool trade press beginning to be regularly quoted using the ‘basis middling’ clause towards the close of 1866 (see for instance: Gore’s General Advertiser, 20 Dec. 1866).

It would probably be correct to describe the years between 1865 and 1873 as ones of flux in the Liverpool forward market with contracts apparently being put to different uses. In this state of flux, a gradual separation took place between on the one hand those transactions involving the sale of specific lots of cotton from a variety of sources, which would normally be delivered, and on the other special contracts for American cotton which did not refer to specific shipments, were made on the basis of a standard quality and which, generally, would be bought back at maturity by the seller. The first surviving rules for forward contracts in the records of the Liverpool Cotton Brokers Association are from 1867. Rule 2 states that ‘In all cases when the terms are by ship or ships, or for shipment before a specified date, the name of the ship or ships ... must be given to the buying Broker ...’ (Liverpool Cotton Brokers Association, Minutes, 23 Aug. 1867, Liverpool Record Office: 380 COT 1/3). This would seem to imply that the contract could be used for a sale on the lines of say 250 bales on a particular ship leaving New Orleans in a named month. On the other hand, the sale might not involve the naming of ships, and simply state a date of future delivery; in other words, it might not refer to actual cotton, and hence it approximated to a futures contract. Indeed, the minutes of the Brokers’ Association seem to suggest strongly that although there was only one standard printed Association contract, sales could be of two distinct types. For instance, the broker Edgar Musgrove in August 1867 referred to ‘... purchases for arrival or future delivery, ...’ (emphasis added) (Liverpool Cotton Brokers Association, Minutes, 16 Aug. 1867, Liverpool Record Office: 380 COT 1/3), and yet there was only one form of standard contract in use. Rules from January 1871 make a similar distinction (see: Rules Relating To Cotton Sold To Arrive, January, 1871, rule 2. Printed insert in Liverpool Cotton Brokers Association, Minutes, Liverpool Record Office: 380 COT 1/5). In March 1871, the President of the Association referred to ‘delivery contracts’ which specified ‘middling American from any ports’. It would therefore seem likely that contracts could be made for future delivery in the late 1860s, or not long after, which did not refer to specific shipments but simply promised to supply a specific quantity by a set date on the basis of one quality; in other words, approximating closely to a fully developed futures contract. The ‘coming of age’ of the Liverpool cotton futures market arrived with the adoption of a separate contract for ‘future delivery’ in 1873. Indeed, a guide to the Liverpool market published forty years later goes as far as to state: ‘Trading in “Cotton Futures” was commenced in 1873.’ (Bruckert, Cotton Pamphlet, p.9). This contract specified the delivery of one hundred bales of American cotton in a fixed month on the basis of middling quality; although, of course, the contract would usually be bought back by the seller rather than the cotton actually being delivered.

7. The Uses of Liverpool Futures Contracts

The mature Liverpool futures contracts could be employed by members of the cotton trade in differing ways. An importer with stocks of cotton in transit to Liverpool, or stored prior to being sold, would use futures to guard against price falls. If the price of cotton fell, an importer might find that the cotton he owned could only be sold for less than he paid for it. To counter this, the importer would sell futures contracts. In other words, he would sell promises to deliver cotton at some date in the future. If the price of cotton fell, he would be selling his actual stock of cotton at a loss but could buy back his futures contracts for less than he sold them for, hence mitigating the loss on the actual ‘spot’ cotton by a profit on the futures contract.

This process of ‘hedging’ with futures required skill and judgement. If a holder of cotton stocks sold too many futures contracts against his stock, he could wipe out all his profit or even make a loss. Hence, importers might decide to ‘hedge’ only a portion of their holdings with sales of futures. Alternatively, they might sell futures contracts promising delivery at a distant date. These distant date contracts could then be employed to ‘cover’ several cargoes, only being bought back if the price of cotton did fall (Cotton, 17 Sep. 1904, p. 9).

It was not only importers who traded futures. Spinners made considerable use of the market. If a cotton spinner held a large stock of cotton he, like an importer, was exposed to the risk of its value falling if the price of cotton declined. Spinners would therefore cover their stocks by selling futures at Liverpool. The price of spun cotton yarn was closely linked to the price of the raw material. Hence, if a spinner held stocks of unsold yarn, he could also cover a proportion of this by selling futures (Todd, Marketing of Cotton, pp. 76, 109, 111).

If a spinner made a contract to spin yarn he might not be able to find the exact type of raw cotton necessary immediately. By the time it was available, the price of cotton might have risen, so upsetting the calculation he had made when quoting the price of finished yarn to the buyer. To avoid this, the spinner could buy futures at Liverpool the moment he struck a yarn contract, knowing that if the price of cotton did subsequently rise, so pushing up the price of the raw cotton he needed, this would be off set by a rise in the value of the futures contracts he held (Todd, Marketing of Cotton, pp. 76, 109, 111).

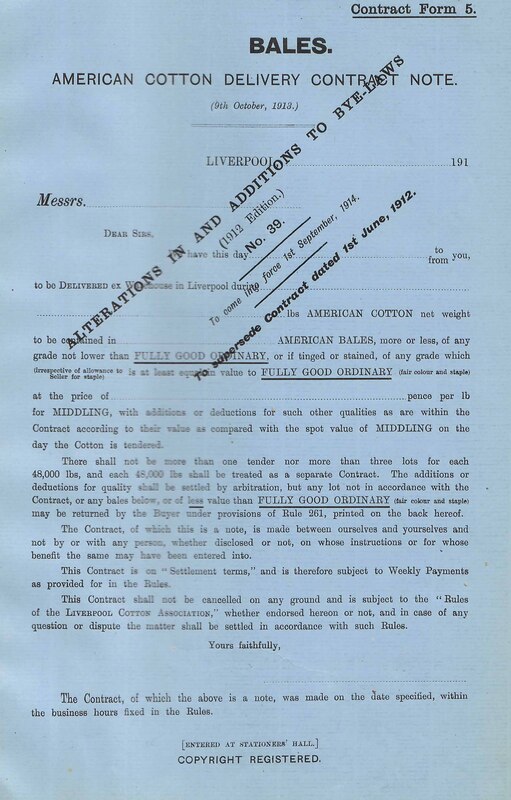

Below:

A Liverpool Cotton

Futures Contract Note

(printed in 1912, and

in author's possession)

A Liverpool Cotton

Futures Contract Note

(printed in 1912, and

in author's possession)

8. The Clearing House and the Development of Margins/Differences

A central feature of all modern futures markets is a clearing house. The clearing house exists to deal with the closing out of contracts - assessing who owes what to whom when contracts are bought back, and overseeing the physical delivery of a commodity in the unusual event that it is actually produced under a futures contract. Of vital importance in a futures market is a system of ‘margins’. Under a futures contract, because a commodity is not set to be delivered until some date in the future, it does not have to be paid for by the buyer, or bought back by the seller until the contract reaches maturity. Anyone, therefore, could enter the market, buying or selling, huge numbers of contracts without having to provide any money and potentially trading far beyond his means. Such a situation is a charter for rampant speculation and instability due to the likelihood of rash traders falling bankrupt when contracts matured. Under a margins system, payments are exchanged regularly between buyers and sellers of contracts between the date when the contract is entered into and the supposed date of ‘delivery’, depending upon whether the value of the commodity in the contract has moved in favour or against the buyer and seller; this ensures that those without adequate means will fail early should the market move against them, before building up a large interest in the market, or be deterred from entering the market in the first place. Margin systems are administered by clearing houses (Veijanovski in Goss, Futures Markets, p. 34. Williams, Function of Futures Markets, p. 14).

The Liverpool cotton market is remarkable for on the one hand developing a clearing house at a very early stage and, on the other, not introducing a margins system until comparatively late - and after considerable destabilizing speculation. The reason for this apparent contradiction lies largely with the broking membership of the Liverpool Cotton Brokers’ Association - the body which regulated the market – which was keen to protect its own financial interests.

The establishment of a clearing house at Liverpool came quickly upon the adoption of a separate contract for futures trading. Confusion appears to have attended the closing of futures at the end of the months specified in the contracts. This was because contracts had been sold and re-sold from trader to trader, often many times, and delays ensued as declarations of cotton were handed on, invoices made etc. Those who had lost by a transaction appear to have deliberately delayed making payment or handing the contract on (Ellison, Cotton Trade, pp. 283-4. Liverpool Cotton Brokers Association, Minutes, 7 Apr. 1873, Liverpool Record Office: 380 COT 1/8). The cotton broker Joseph Morgan therefore suggested to the Liverpool Cotton Brokers Association in the spring of 1873 that it should create a special clearing house to oversee the swift closing out of contracts. Despite some opposition from brokers who feared such an institution would facilitate information about their own firms’ business becoming known, the clearing house was established for a trial period. Essentially, it simply required all futures contracts falling due in a particular month to be presented in one place on one day and this to be overseen by a special committee of the brokers’ association. This worked well and the experiment was repeated; by June 1873, a permanent home for the clearing house was being sought (Ellison, Cotton Trade, p. 281. Liverpool Review, 11 June 1887, p. 10. Liverpool Cotton Brokers Association, Minutes, 7, 18 Apr. 1873, Liverpool Record Office: 380 COT 1/8). The first clearing house for commodities, not only in Britain but anywhere in the world, had been created. Within a couple of years, the Clearing House had its own printed rules, premises and an elected committee, subject to the brokers’ association, which oversaw the clearing, and settled disputes. All futures contracts had to pass through it, and any broking firm could be fined if it did not send a representative to a clearing involving contracts it was party to (Liverpool Cotton Brokers Association, Constitution, Rules and Regulations of the Clearing House for Arrival and Delivery Contracts, (Liverpool, 1876) in the Bodleian Library, Oxford: 1784 e. 18 (1)).

Despite the pioneering development of the Clearing House, the development of a system of margins at Liverpool took a surprisingly long time; even though there was considerable and early disquiet on this subject. The first evidence of concern in Liverpool regarding the extent and standing of forward trading can be found as early as 1863. The broking firm of Smith, Edwards & Co. commented at the end of the year 1863: ‘The system of business in use gives boundless facilities to the operations of speculators without capital, and it cannot be doubted that if a great breakdown in the market occurred immense confusion would follow’ (see: Smith, Edwards & Co., Annual Circular for 1863, in the Liverpool Record Office: MD 230-22). The brokers Ellison & Heywood argued at the same time that using forward sales ‘... men of limited capital and others of no means whatever ...’ were able to operate in the market, and that should prices fall, they would never be able to fulfill their engagements; something needed to be done to put the market upon a sounder footing (see: Circular of Ellison & Heywood, reprinted in The Economist, 20 Feb. 1864, supplement, p. 27). Other brokers and merchants echoed these sentiments (see for instance: Anonymous letter in The Times, 12 Nov. 1863, p. 6 and 11 Dec. 1863, p. 4).

A system whereby buyers of contracts paid a deposit into a separate bank account was put forward by some merchants and cotton broking firms including Ellison & Heywood and Smith, Edwards & Co (see for instance: Circular of Ellison & Heywood, reprinted in The Economist, 20 Feb. 1864, supplement, p. 27. Smith, Edwards & Co.’s Annual Circular. Anonymous merchant in, The Times, 12 Nov. 1863, p. 4, 11 Dec. 1863, p. 6). However, the objections raised were several. It was suggested that a deposits system was impractical given the need for new bank accounts to be opened and closed, perhaps quickly if contracts were resold. Speculators (who bought the forward contracts) argued that the selling merchants should also be required to make deposits, for it was contended that sellers embarked upon ‘bear’ selling and hence ‘gambled’ as much as the so-called speculators. In addition, it was stated that a deposit system would lock up too much capital. A meeting of Liverpool cotton brokers discussed the idea; a merchant commented that while the brokers did not challenge the justice of the proposed reform ‘refuge was taken in the alleged impracticability of the measure proposed’, though the merchant suspected that the loss of the ‘gambling clientèle’ (and their brokerage payments) in fact gave rise to the brokers’ reluctance. The merchant went on to warn that if nothing was done a commercial crisis greater than 1847 or 1857 was in prospect (Anonymous merchant in, The Times, 12 Nov. 1863, p. 4, 11 Dec. 1863, p. 6., 14 Dec. 1863, p. 9).

In fact, the following year, 1864, witnessed something of a crisis in this emerging market. A sharp downturn in the price of cotton in the early autumn brought panic and numerous bankruptcies; market commentators noted that the rampant and insecure forward trading of those with limited means had greatly exacerbated the crisis in the market (Circular of Ellison & Heywood, reprinted in The Economist, 11 Mar. 1865, supplement, pp. 21-2. Gore’s General Advertiser, 1, 8, 29 Sept., 13 Oct. 1864; 5 Jan. 1865). Despite this salutary lesson, no action was taken. The lack of action on the part of the Liverpool Cotton Brokers Association on the question of margins indicates one of the weaknesses this early body had in acting as the regulatory body for the developing futures market. It was not a body encompassing all concerned with the market, but only the brokers. Specifically, the merchants and spinners were not members. Hence while merchants, and later spinners, desired at different times to see the creation of a margins payments system, the interests of the brokers could and did prevent this: the more forward and futures trading there was, the more brokerage they would earn on these transactions. If a broker traded a contract for an individual who went bankrupt, the most he could lose was a brokerage payment - so long as he had not extended any credit to the person concerned.

Over the next two decades, proposals for deposit and margins systems were put forward but not adopted, for instance in 1870 and 1877, and a system of optional deposits was endorsed in 1870 but appears not to have been used. Comments at brokers’ meetings highlighted a number of objections, similar to those voiced in 1863, with one important concern being a desire on the part of a group of the brokers not to limit the extent of the market. Interestingly, some of the more conservative brokers opposed schemes because they believed it would in some way aid speculation; quite how, is not clear. Other cotton brokers (particularly those with slender resources) who imported cotton and hedged it using futures did not wish to see their capital tied up; this latter issue affected some merchants who, hence, also opposed a margins system (Liverpool Cotton Brokers Association, Minutes, 30 Sept., 7, 14, 28 Oct. 1870, in the Liverpool Record Office: 380 COT 1/5; 13 Apr. 1877, 380 COT 1/10. Letter of Thomas Holder, 1 Oct. 1870 inserted in ibid., 380 COT 1/5. American Chamber of Commerce in Liverpool, Minutes, 12, 31 Oct. 1870, in the Liverpool Record Office: 380 AME 3. Ellison, Cotton Trade, pp. 292-3. The Porcupine, 28 May 1870, p. 88 - The Porcupine was a Liverpool satirical magazine).

Pressure for change built up outside the market. Observers were shocked by the possibilities which the lack of a deposit system permitted. The Porcupine, a satirical Liverpool publication, declared as early as 1870: ‘An American, fresh over from the other side, with scarce enough credit at home to buy “a suit of clothes,” can promenade our [Exchange] Flags within four-and-twenty hours after his arrival the owner of some thousand bales of cotton.’ The author recommended a deposit system on the model of that already used in the New York cotton market, but suspected that brokers wished to maintain their incomes at the level of the price-inflated Civil War and were hence keen not to reduce speculation (The Porcupine, 28 May 1870, p. 88). Other commentators argued in a similar vein (See for instance: William B. Halhed, ‘On Commercial Corners’ in The Nineteenth Century, X, Oct. 1881, p. 535).

The facility which futures gave to speculators led spinners to propose, in 1881, at a joint meeting with the brokers’ association, the adoption of a monthly settlement of ‘differences’ or margins between buyers and sellers of futures. The brokers stated that they were, in fact, willing to adopt the payment of differences and were keenly looking into it, though how representative of the majority in the association the deputation’s views were is open to question given the earlier opposition from brokers to such a move. However, they stated that in the past, spinners, who were already making use of futures, had objected to this (evidence for this is hard to find although it is possible that some spinners using futures might have objected because it would tie up capital). The brokers also stated that there were problems in designing a system which did not place ‘... very serious difficulties in the way of legitimate business ...’ (no doubt the importing activities of brokers and brokerage income). The spinners left the meeting feeling dissatisfied (see: Letter to the Chairman of the Manchester Cotton Spinners’ Association, 1881, inserted in Liverpool Cotton Brokers Association, Minutes, 4 Dec. 1881, in the Liverpool Record Office: 380 COT 1/13. The Times, 20 Oct. 1881, p. 6).

The deadlock was broken by the activity of an American speculator, Morris Ranger. Through buying up futures contracts he managed to corner the Liverpool market in 1879, attempted it in 1880, managed to do so again in 1881 and fell spectacularly bankrupt in 1883 with estimated debts in Liverpool of £400,000. In the process, his speculations had forced up the price of the industry’s raw material, to the considerable discomfort and anger of the spinners. The remarkable point was that Ranger had been to all intents and purposes bankrupt long before he finally declared the fact publicly in October 1883; the lack of a system of margins in Liverpool had permitted him to continue trading as he tried to extricate himself from his losses, but in fact storing up mounting losses for the date when he could continue to trade no longer (Thomas Ellison, Gleanings and Reminiscences, (Liverpool, 1905), pp. 337-42. W. W. Biggs, ‘Cotton Corners’ in Transactions of the Manchester Statistical Society, (1894-5), pp. 128-9. The Times, 2 Nov. 1883, p. 10, 3 Nov. 1883, p. 7. Bank of England, Liverpool Letter Book, 31 Oct., 2 Nov., 1883 in the Bank of England archive, London: C129/27).

Below:

Portrait of Morris Ranger,

A Cotton Speculator who

"Cornered" the Liverpool Cotton

Market in 1879 and 1881

before falling bankrupt in 1883

(from: "The Graphic",

8 October1881)

Portrait of Morris Ranger,

A Cotton Speculator who

"Cornered" the Liverpool Cotton

Market in 1879 and 1881

before falling bankrupt in 1883

(from: "The Graphic",

8 October1881)

In Liverpool the extremity of the situation was clearly identified as the result of a lack of a margins system and it was reported that, in consequence, support in the market for adopting a margins system similar to that used in New York was gaining ground (see: The Times, 1 Oct. 1881, p. 9; 6 Oct. 1881, p. 4; 31 Oct. 1883, pp. 5, 9; 1 Nov. 1883, p. 10; 2 Nov. 1883, p. 10; 3 Nov. 1883, p. 7; 23 Nov. 1883, p. 7. Liverpool Echo, 28 Oct. 1929). Despite this, opposition still existed among the brokers. Many did not wish to see a possible contraction of the futures market - it should perhaps be noted that one source states that Ranger paid no less than the enormous sum of £330,000 to brokers in Liverpool from September 1878 to his collapse in 1883 (The Times, 23 Nov. 1883, p. 7).

A group of about sixty Liverpool brokers keen to avoid the dangers of the existing situation began a ‘Settlement Association’ for paying margins on a voluntary basis in December 1882, independent of the Liverpool Cotton Association (which had now succeeded the old brokers’ association). Every two weeks a special committee established the ruling price of futures, with cash being transferred between members of the Settlement Association depending upon whether prices for futures had moved in their favour or against them. The Settlement Association ran independently for two years, during which time the practicality of the system was demonstrated. According to one source, members of the Settlement Association attracted more futures business because settlements gave greater security. At the end of this two-year period, the new Liverpool Cotton Association (a body which admitted merchants to full membership and spinners to associate membership) adopted the scheme officially, but even at this stage the proviso that it was only voluntary remained, although the vast majority used it - no doubt bearing in mind the Ranger episode and the success of the Settlement Association (The Times, 23 Nov. 1883, p. 7. Ellison, Cotton Trade, pp. 294-6. A. Bryce Muir, Cotton Futures: A Collection of Articles on a Technical Subject, (Liverpool: Wood & Sloane Ltd., 1936), pp. 22-3).